66 Lottery Deposit, 66 Lottery Withdrawal and withdrawal-problem records

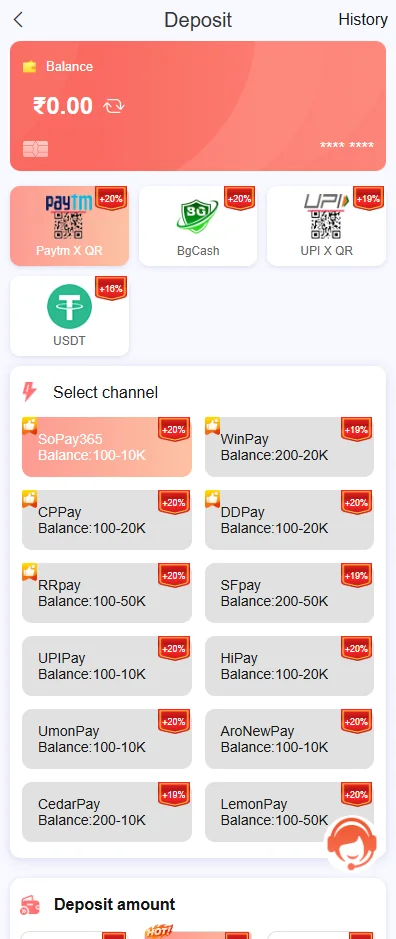

The current deposit interface shows Paytm X QR, BgCash, UPI X QR and USDT near the top. A larger list of selectable channels appears below, each with its own visible range or label.

Choose a channel only after checking whether the intended amount falls inside the displayed range. A route showing a minimum and maximum can reject an amount outside that interval.

Payment methods can change inside the platform. Always rely on the live account screen rather than an old screenshot or message.

For the broader 66 Lottery overview and the other account sections, return to the 66 Lottery homepage after finishing this 66 lottery deposit withdrawal topic.

Using QR and UPI channels carefully

A QR or UPI route may generate payment instructions after the amount is selected. Match the exact amount and verify the payee information displayed by the live channel.

Keep the bank or wallet transaction reference after payment. It can help match the request with Deposit History if the platform balance does not update immediately.

Do not send funds to a personal number received through an unrelated chat. Open the payment route from the current deposit screen.

USDT and other wallet methods

The supplied screen includes USDT as a deposit choice and USDT TRC20 on the withdrawal side. Network and address accuracy matter for token transfers.

Confirm the network shown by the platform before sending. A transfer on the wrong network or to the wrong address may not be recoverable.

Copy the address directly from the live screen and verify the opening and closing characters before approving a transaction.

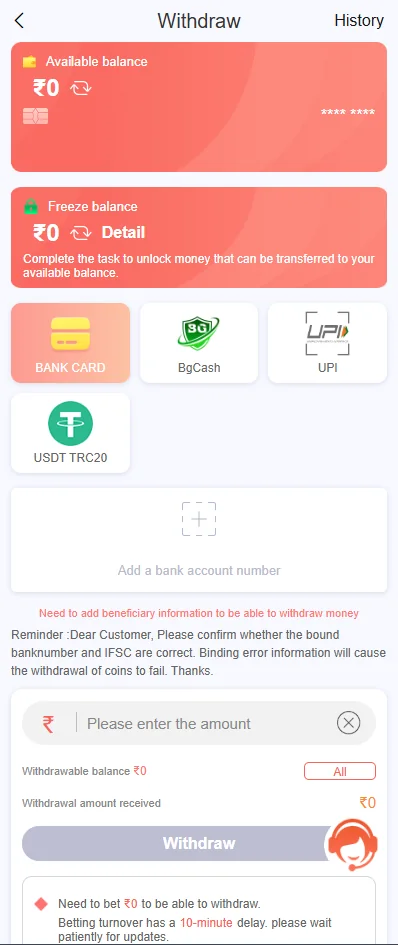

Available balance and frozen balance

The withdrawal screen separates available balance from frozen balance. A total visible elsewhere in the account may include funds that are not currently eligible for withdrawal.

Frozen funds can relate to a pending transaction, an account condition or another platform rule. Read the message attached to the balance instead of assuming the funds have disappeared.

Deposit money, game balance and activity rewards may not all become withdrawable under the same conditions.

Adding beneficiary information

The withdrawal interface asks the user to add beneficiary details. The visible note refers to account name, bank account number and IFSC information.

Enter details that belong to the intended beneficiary and check every digit before saving. A mismatched name or account number can lead to a rejected or failed request.

UPI and wallet withdrawals can also require a correctly linked identifier. Do not reuse beneficiary details copied from another person.

Why a withdrawal can remain unavailable

The Withdraw button can remain disabled when no beneficiary is added, the available balance is below the current minimum, funds are frozen or another account condition is incomplete.

Review the live message, beneficiary status and withdrawal history before making another request. Repeated submissions can create multiple pending records without solving the original issue.

No fixed processing time is promised on this page. The status shown by the current account and payment channel is the relevant source.

Transaction records and account security

Use Deposit History and Withdrawal History to confirm the amount, request time and current status. Save the reference number without sharing the full bank or wallet details publicly.

Never provide a password or one-time code to someone who claims that it is required to release a withdrawal. Authentication codes are for account access, not for proving ownership to an unknown person.

If account details change without permission, stop new transactions and secure the account before continuing.

Matching a payment with the account record

A bank or wallet confirmation shows that money left the payment account, while Deposit History shows whether the platform matched it with the 66Lottery account. Both records are useful when checking a delay.

Compare the amount, time, channel and reference. A mismatch in any of these fields can explain why a payment has not appeared in the expected balance.

Understanding withdrawal status stages

A withdrawal can move through states such as submitted, pending, approved, failed or completed depending on the live platform. The exact words may differ, but the history record should be checked before repeating the request.

A completed status should be compared with the receiving bank, UPI or token wallet. If the platform shows failure, confirm whether the balance returned before attempting another withdrawal.

Keeping transaction evidence safely

Save the transaction ID, amount, time and channel, but hide the full bank account, wallet address, phone number and QR code before sharing a screenshot.

Evidence is most useful when it is complete enough to identify the transaction without exposing account access. Passwords and OTPs should never be included.

Choosing a channel by method, not only by banner

Deposit pages can highlight one route while listing several alternatives below. Choose based on the available account, displayed range and current instructions rather than the most colourful banner.

A channel name can include a QR, UPI, wallet or token route. Confirm which payment application or network is expected before proceeding.

Minimums, maximums and entered amounts

A displayed range can be enforced by the payment processor. Entering less than the minimum or more than the maximum may prevent the order from being created.

Do not split a payment into repeated smaller transfers unless the live instructions specifically permit it. Multiple unmatched transfers are harder to reconcile.

Beneficiary edits and withdrawal safety

Treat a beneficiary change as a security-sensitive action. Recheck the name, account number, IFSC, UPI identifier or token address after saving.

If a saved beneficiary changes without permission, secure the account before requesting a withdrawal. Do not assume the platform will automatically detect the wrong destination.

Match every wallet order with one complete record

Before paying, note the account, amount, selected channel and order or reference information shown on the platform. After payment, retain the bank, UPI or wallet confirmation without exposing private credentials.

The payment proof and the platform order should refer to the same amount and time. A screenshot from another transaction does not establish that the current account order was completed.

Do not send a second payment merely because the balance has not refreshed. First check the order record, refresh the account once and wait for the status to update.

Read pending, failed and completed as different states

Pending means the request has not reached a final state. Failed indicates that the platform or payment route did not complete the order. Completed should be checked against both the platform record and the external payment account.

A frozen balance, turnover requirement, beneficiary check or minimum amount can affect withdrawal availability. Read the exact on-screen message before changing payment details.

When a status changes unexpectedly, preserve the earlier and later screens with dates and personal details hidden. This creates a clearer timeline for support.

Protect beneficiary and payment details

Enter beneficiary information directly inside the verified account route. Avoid sending full bank details, UPI PINs, OTPs or private wallet keys through chat messages.

Check the account holder name, number, UPI ID or network address before submission. Small differences can send a withdrawal to the wrong destination or cause rejection.

If an unfamiliar beneficiary is already saved, stop the transaction and secure the account before editing or adding another method.